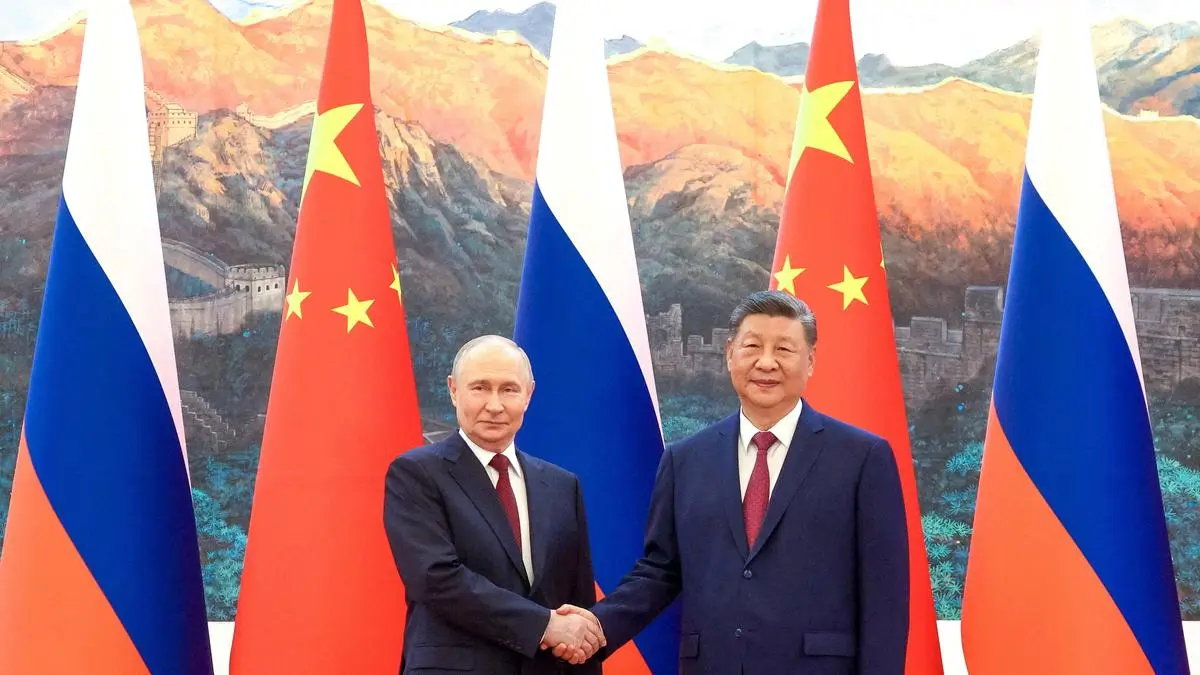

Beijing has emerged as the clear clearinghouse for global strategic liabilities. Within a single multi-day window, Chinese leader Xi Jinping hosted United States President Donald Trump for intense closed-door negotiations, only to immediately roll out the red carpet for Russian President Vladimir Putin. Mainstream analysis views this rapid sequencing as mere diplomatic optics or a display of superpower prestige. This perspective misses the underlying mechanics. Beijing is executing an explicit strategy of geopolitical arbitrage, exploiting the asymmetrical dependencies of two isolated or volatile nuclear powers to maximize its own strategic autonomy.

By operating as the central node between a highly transaction-oriented Washington and an economically captive Moscow, China is converting its geopolitical position into hard economic and strategic concessions. The structural mechanics of this three-body problem reveal how Beijing is optimizing its position.

The Tri-Causal Framework of Chinese Strategic Autonomy

Beijing’s foreign policy does not operate on ideology or permanent alliances; it operates on a calculus of balancing dependencies. The simultaneous engagement with Trump and Putin can be broken down into three distinct operational vectors.

1. The De-escalation Buffer with Washington

The primary objective during Trump's visit was stabilizing the world’s most critical bilateral trade relationship amidst severe exogenous shocks, specifically the escalating US-Iran conflict and disruptions in the Strait of Hormuz. For Beijing, a volatile United States under a transaction-first executive presents an unpredictable tariff and sanctions risk. By positioning itself as a mediator capable of absorbing billions in American agricultural goods while holding the key to diplomatic outcomes in the Middle East, China creates an economic circuit breaker. This relationship is strictly transactional, defined by short-term concessions designed to prevent structural decoupling.

2. The Asymmetrical Dependency Monopsony Over Moscow

Conversely, the relationship with Moscow is structurally locked into a monopsony framework. Sanctions imposed by Western powers have systematically severed Russia from global capital markets, leaving China as its primary economic lifeline. Putin's arrival in Beijing—backed by a massive delegation including five deputy prime ministers and eight cabinet ministers—is not a meeting of equals. It is a negotiation between a distressed asset vendor and a highly capitalized buyer. China utilizes this leverage to extract deep discounts on primary inputs, specifically crude oil and natural gas, while dictating the terms of bilateral settlement.

3. The De-dollarization Infrastructure Build-out

The structural foundation underlying the Sino-Russian alignment is the creation of financial plumbing entirely insulated from Western sanctions. By shifting bilateral trade almost exclusively to the renminbi (RMB) and the rouble, Beijing is utilizing Russia as a live testing ground for its Cross-Border Interbank Payment System (CIPS). This reduces China's vulnerability to potential future Western sanctions and builds an alternative global financial network that bypasses the SWIFT system entirely.

Quantifying the Sino-Russian Economic Cost Function

The power dynamic between Beijing and Moscow is clearest in the trade data. Bilateral trade between the two nations surpassed $240 billion, more than doubling pre-Ukraine war baselines. However, the composition of this trade reveals a profound structural imbalance that favors Chinese industrial policy at the expense of Russian economic sovereignty.

+-----------------------------------------------------------------------+

| SINO-RUSSIAN SYMMETRY BREAKDOWN |

+-------------------------------------------------+---------------------+

| Russian Exports to China | % of Total Volume |

+-------------------------------------------------+---------------------+

| Crude Oil, Liquefied Natural Gas (LNG), Coal | ~75% |

+-------------------------------------------------+---------------------+

| Raw Timber and Mineral Commodities | ~15% |

+-------------------------------------------------+---------------------+

| Agricultural and Other Goods | ~10% |

+-------------------------------------------------+---------------------+

| | |

+-------------------------------------------------+---------------------+

| Chinese Exports to Russia | % of Total Volume |

+-------------------------------------------------+---------------------+

| Dual-Use Industrial Machinery & Microelectronics| ~40% |

+-------------------------------------------------+---------------------+

| Automotive Vehicles and Transport Equipment | ~35% |

+-------------------------------------------------+---------------------+

| Consumer Electronics and End-Use Manufactures | ~25% |

+-------------------------------------------------+---------------------+

This trade matrix demonstrates that Russia has effectively been relegated to a resource appendage for the Chinese industrial base. China now absorbs an estimated 50% of Russia’s total crude oil exports. In a classic monopsonistic market structure, the buyer possesses the leverage to dictate prices. Because Russia cannot easily reroute its fixed pipeline infrastructure toward Europe, Beijing successfully demands steep discounts below the Brent crude benchmark.

Furthermore, the operational mechanics of the 47-page joint statement and the 40 cooperation agreements signed during Putin's visit focus heavily on deepening this energy asymmetry. While Russia secures short-term fiscal survival via energy rents, China secures long-term resource abundance at sub-market rates, all while paying in its own currency.

The Strategic Bottleneck of Dual-Use Microelectronics

A critical friction point in this trilateral dynamic is the transfer of Chinese technology to the Russian defense-industrial base. The United States has repeatedly threatened secondary sanctions against Chinese financial institutions that facilitate the flow of high-tech components to Russia.

Beijing’s response to this threat is an exercise in risk-managed friction. Rather than halting the supply of vital industrial goods, China has systematically diversified its supply chains through third-party intermediaries in Central Asia and the South Caucasus. The operational mechanism relies on a decentralized network of small, non-systemic Chinese banks that do not have exposure to the US clearing system.

[Chinese Tier-1 Manufacturers]

│

▼ (Non-Sanctioned Industrial Component Sales)

[Domestic Shell Distributors / Tier-3 Regional Banks]

│

▼ (Cross-Border Renminbi Clearance via CIPS)

[Central Asian Intermediaries (Kazakhstan/Kyrgyzstan)]

│

▼ (Re-export / Transshipment)

[Russian Defense-Industrial Procurement Entities]

This structural workaround ensures that even if Washington enforces secondary sanctions, China's core financial institutions remain unexposed. This allows Beijing to continue supplying Russia with critical dual-use items—such as computer numerical control (CNC) machine tools, semiconductor components, and optical equipment—without crossing the threshold that would trigger a systemic economic confrontation with the West.

Middle East Vulnerabilities and the Strait of Hormuz Leverage

The sudden intersection of Trump’s and Putin’s visits with the escalating US-Iran conflict highlights the complex theater of maritime logistics. The primary systemic threat to the global economy is the potential closure of the Strait of Hormuz, driven by the ongoing conflict and the American seizure of Iranian ports.

For Beijing, the Strait of Hormuz represents a critical energy vulnerability. China imports roughly 40% of its crude oil from the Persian Gulf. A protracted blockade would force China to draw down its Strategic Petroleum Reserves (SPR) and rapidly accelerate domestic rationing. This vulnerability explains Beijing's dual-track diplomacy.

By engaging with Trump, Xi Jinping positioned China as a necessary diplomatic weight capable of pressuring Tehran to de-escalate, leveraging its status as Iran’s largest economic partner. Simultaneously, by hosting Putin immediately afterward, Xi secured a contingency plan.

If the Persian Gulf shuts down completely, Russia’s land-based energy pipelines—such as the Eastern Siberia–Pacific Ocean (ESPO) pipeline and the Power of Siberia gas network—become China's primary shield against maritime blockades. Putin’s weakness on the global stage allows Beijing to demand that Russia maximize the throughput of these land-based corridors, transforming a global maritime crisis into a structural win for Chinese energy security.

The Illusion of Alliance: Structural Constraints of the Axis

Despite the grand rhetoric of an "unyielding" partnership and an "unprecedented level" of cooperation, the Sino-Russian relationship lacks the institutional integration of a true military alliance like NATO. The relationship contains three fundamental limitations:

- Asymmetrical Risk Appetite: Moscow seeks to dismantle the existing international security architecture because it operates under a regime of survival amid isolation. Beijing, conversely, is the primary beneficiary of the globalized economic order. It seeks to reform international institutions to match its power, not to destroy them. China will not risk its access to Western consumer markets to bail out Russian military campaigns.

- The Strategic Central Asian Conflict: Beneath the surface of cooperation, Beijing and Moscow are competing for influence in Central Asia. Through its Belt and Road Initiative, China has systematically displaced Russia as the dominant economic power in former Soviet republics, converting Moscow’s traditional sphere of influence into a corridor for Chinese logistics.

- The Technology Transfer Threshold: While China provides dual-use components, it carefully restricts the transfer of its most advanced military tech. Beijing treats its domestic semiconductor chips, aerospace engineering, and artificial intelligence capabilities as proprietary strategic leverage, ensuring that Russia remains a generation behind Chinese capabilities.

The Strategic Play

The operational reality of the current geopolitical landscape demands that corporate strategists, risk officers, and defense analysts abandon the binary view of global power. Beijing is not forming an axis with Russia, nor is it seeking a grand bargain with the United States. It is operating a highly sophisticated, data-driven hedging strategy designed to extract maximum resources from the weak while deflecting regulatory and military pressure from the strong.

The immediate strategic move for organizations navigating this landscape requires three distinct steps:

- De-risk Financial Supply Chains from RMB Clearing Networks: As China and Russia expand non-dollar clearing mechanisms via CIPS, expect the US Treasury to aggressively expand the scope of secondary sanctions. Firms must audit their tier-2 and tier-3 suppliers for any operational exposure to regional Chinese banks handling transshipments through Central Asia.

- Hedge for Structural Energy Re-routing: The deepening dependency of Russia on Chinese energy markets means that land-based pipeline capacities to the East will be locked up long-term. Global energy desks must price in a permanent structural discount for Russian Urals in the East, while preparing for heightened volatility in maritime Brent and WTI crude should Middle Eastern choke points face further military disruptions.

- Anticipate the Targeted Tariff Vector: Trump’s transactional approach to Beijing will likely result in short-term agricultural purchasing agreements, but these agreements will mask structural restrictions on Chinese high-tech exports. Advanced manufacturing firms must accelerate the diversification of assembly and component sourcing away from China, particularly in sectors reliant on dual-use microelectronics and heavy machinery.

Beijing has demonstrated that it holds the structural cards in this trilateral dynamic. By acting as the sole actor capable of speaking authoritatively to both Washington and Moscow, China has insulated its economy from the immediate fallout of both the Ukraine and Iran conflicts, turning its competitors' geopolitical vulnerabilities into its own long-term structural leverage.